| Practice area: | Behavioural Economics | Finance |

|---|---|

| Client: | N/A |

| Published: | 26 January, 2023 |

| Keywords: | AE auto enrolment pension |

Calum Kennedy at London Economics reflects on the success of the auto-enrolment scheme in the UK and lays out some of the challenges for the road ahead…

In October 2022, the UK auto-enrolment (AE) pension scheme celebrated its tenth anniversary. Over the past ten years, the pensions landscape in the UK has changed markedly. AE has been successful in narrowing enrolment gaps across income, occupation, and age groups. Total pension savings have increased in real terms, and many employers go beyond the stipulated minimum contribution rates. However, challenges remain for the coming decade, including ongoing participation deficits for self-employed workers, multiple job holders, and some demographic groups.

Auto-enrolment in the UK

Auto-enrolment was introduced following the Pensions Act 2008 and was intended to address declining workplace pension provision in the early 2000s.[1] The scheme stipulates that every UK employer must register eligible employees (aged between 22 and state pension age, and earning over £10,000 per year) into a workplace pension. AE was phased in between 2012 and 2017, starting with the largest employers. Since 2018, all UK businesses have had to provide a workplace pension to new employees.

Both employers and employees are subject to minimum contribution rates. These minimums were also phased in over time, starting at 2% of qualifying annual earnings. Following increases in 2018 and 2019, the current minimum contribution stands at 8% of total qualifying annual earnings, of which 3% must come from the employer and 5% from the employee.[2]

Narrowing enrolment gaps

In the UK, auto-enrolment’s most celebrated success has been in increasing overall workplace pension enrolment rates. Since the scheme’s inception, over 10.6 million workers have been enrolled into a workplace pension, meeting targets set out by the Pensions Commission in 2006.[3] Most of these gains have been accrued in the private sector, which has typically been characterised by lower enrolment rates than the public sector. Since 2012, enrolment rates amongst eligible employees in the private sector have more than doubled, from 42% to 86%.[4] As a result, private sector workplace pension enrolment rates now rival those of the public sector (as shown in Figure 1).

| Figure 1 Percentage of eligible employees participating in workplace pension by sector |

|

| Source: Adapted from Department for Work and Pensions (2022). |

There has also been a convergence in enrolment rates across incomes, age groups, and occupations. In 2012, the gap in enrolment between those on the highest incomes (more than £60,000 per annum) and the lowest incomes (between £10,000-£20,000 per annum) was 49%. Less than one third of the lowest income employees were enrolled in a workplace pension, as opposed to 81% of the highest income employees. By 2021, the enrolment gap had fallen to 11%.[5]

Historically, private pension wealth has been more unequally distributed than total wealth in the UK.[6] However, increased workplace pension enrolment amongst lower income employees is helping to reduce this disparity. Between 2016 and 2020, the percentage of total private pension wealth held by households in the bottom five income deciles increased by around 4%, whilst the share held by the top income decile fell by roughly 1.5% (Figure 2).[7] By increasing participation in workplace pensions among lower income groups, AE is helping to reduce income inequality in older age.

| Figure 2 Percentage of total private pension wealth held, by household net income decile |

|

| Source: Adapted from Office for National Statistics (2022). |

There has been similar success in increasing engagement amongst younger people and workers in elementary professions – groups with previously low participation rates. Workplace pension enrolment amongst the youngest qualifying age group (22-29) rose from 39% in 2012 to 86% in 2021. Over the same period, the gap in enrolment between professional and elementary occupations fell from 44% to 7%.[8]

Increased total savings

Rising participation rates have led to an increase in aggregate pension contributions and pension wealth. Since 2012, total workplace pension contributions have risen in real terms, from £81.7bn to £114.6bn. Total annual savings for eligible employees increased across all occupations in the private sector, and for both male and female employees.[9]

The rise in total contributions is perhaps unsurprising, given AE’s success in increasing workplace pension uptake. Potentially of more interest is the effect of AE on individual contributions. In the public sector, the effect has been muted – annual pension contributions per eligible employee rose slightly from £6,030 in 2012 to £6,950 in 2021.[10]

Going beyond minimum contribution rates

Minimum contribution levels are a key feature of AE. These contribution levels effectively serve as a ‘default’ option for employers and employees when setting up pension contributions. Default levels matter. A large literature in behavioural economics shows that people often exhibit status quo bias – a tendency to prefer the maintenance of the current state of affairs (see here for a helpful primer on status quo bias, alongside other behavioural economics insights). The propensity of individuals to stick with default choices has led to concerns that the current AE minimum contribution rates are reducing contribution rates amongst people who would otherwise have saved more.[11]

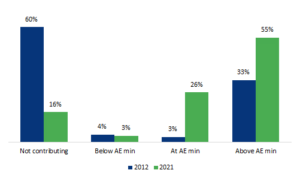

Encouragingly, many employees and employers appear to be going beyond minimum contribution rates. In 2012, 33% of eligible private sector employees were contributing above the current minimum level of 8% of total qualifying earnings (Figure 4). By 2021, over half of all eligible employees were contributing above the AE minimum. The increase in the proportion of employees contributing above the AE minimum was observed across all occupation classifications and economic sector types.[12]

| Figure 3 Percentage of eligible private sector employees by contribution level |

|

| Source: Author’s calculations based on data from the Department for Work and Pensions (2022) and Office for National Statistics (2022). |

The road ahead

Since its inception, AE has recorded numerous successes. Enrolment rates have increased, particularly in previously under-represented sectors and demographic groups. Total pension savings have increased, reducing inequality in private pension wealth. Many employees continue to save above the statutory minimums.

However, there remain challenges for the road ahead. It has been five years since the last major review of AE, but inequalities in enrolment continue to exist.[13] AE’s current eligibility criteria often excludes some groups, including the self-employed and multiple job holders.[14] There are still participation gaps between demographic groups, with women and ethnic minorities under-represented.[15],[16] Some commentators have voiced concerns that minimum contribution rates remain too low. The Association of British Insurers, for example, advocates for an increase in minimum contributions to 12% of qualifying earnings.[17] As AE enters its second decade, policymakers will need to capitalise on the momentum of its first decade to address these challenges and ensure a workplace pension scheme that works for all.

Calum Kennedy is an Economic Analyst at London Economics. He recently completed an MPhil in Economics at the University of Cambridge and holds a BSc in Economics from the University of St Andrews. He can be contacted at [email protected].

LE’s Financial Services team

The London Economics Financial Services teams, led by Patrice Muller, has a long and proven track record of advising private and public clients on financial sector issues through theoretical and empirical economic analysis of wholesale and retail financial markets, financial sector policy and financial institutions. Drawing on our team’s expertise on pensions and the financial sector more widely, as well as our rigorous and innovative research approach, we have provided market analyses, policy recommendations and expert witness work for HMRC, the British Business Bank, the British Insurance Brokers’ Association, the European Commission, national governments, as well as private sector clients. One of our recent pieces of work is a study for the European Commission’s Directorate-General for Financial Stability, Financial Services and Capital Markets Union (DG FISMA), identifying best practices that should to be followed when implementing an auto-enrolment pension scheme. For further examples of work please visit: https://londoneconomics.co.uk/finance. You can reach Patrice and Calum directly at [email protected].

LE’s Behavioural Economics team

We have a dedicated team of behavioural economists who have extensive international expertise in behavioural insights within the financial sector. Lead by Dr Charlotte Duke and James Suter, our behavioural experts have advised the European Insurance and Occupational Pensions Authority, the European Commission, the UK Financial Conduct Authority and private sector banks in the UK, Europe and internationally. We work with our clients using behavioural insights in customer communications, product framing and design, and customer journey mapping. Using behavioural insights we increased pension savings re-investment by over 100% for a large pensions provider in South Africa How to Double Savings Rates: A Case Study in Nudging for Good (Our work is bespoke to our clients’ needs, and helps our clients achieve both policy and business objectives. For further examples of our work please visit https://londoneconomics.co.uk/behavioural. You can reach James and Charlotte directly at [email protected].

[1] Association of British Insurers. (2022). “Automatic Enrolment: What will the next decade bring?” https://www.abi.org.uk/globalassets/files/publications/public/lts/2022/automatic-enrolment-what-will-the-next-decade-bring/.

[2] Department for Work and Pensions. (2020). “Automatic enrolment evaluation report 2019.” https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/883289/automatic-enrolment-evaluation-report-2019.pdf.

[3] Department for Work and Pensions. (2022). “Review of the automatic enrolment earnings trigger and qualifying earnings band for 2022/23: supporting analysis.” https://www.gov.uk/government/publications/automatic-enrolment-review-of-the-earnings-trigger-and-qualifying-earnings-band-for-202223/review-of-the-automatic-enrolment-earnings-trigger-and-qualifying-earnings-band-for-202223-supporting-analysis.

[4] Department for Work and Pensions. (2022). “Workplace pension participation and savings trends of eligible employees: 2009 to 2021.” https://www.gov.uk/government/statistics/workplace-pension-participation-and-savings-trends-2009-to-2021.

[5] Ibid.

[6] Office for National Statistics. (2022). “Saving for retirement in Great Britain: April 2018 to March 2020.” https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/pensionwealthingreatbritain/april2018tomarch2020#measuring-the-data.

[7] Office for National Statistics. (2022). “Pension wealth: wealth in Great Britain.” https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/datasets/pensionwealthwealthingreatbritain.

[8] Department for Work and Pensions (n. 4).

[9] Department for Work and Pensions. (2022). “Ten years of Automatic Enrolment in Workplace Pensions: statistics and analysis.” https://www.gov.uk/government/statistics/ten-years-of-automatic-enrolment-in-workplace-pensions/ten-years-of-automatic-enrolment-in-workplace-pensions-statistics-and-analysis#the-amount-saved-into-workplace-pensions.

[10] Department for Work and Pensions (n. 4).

[11] The Investing and Saving Alliance. (2020). “Getting Retirement Right: Plan, Prepare, Enjoy.” https://www.tisa.uk.com/wp-content/uploads/2020/02/Getting-Retirement-Right.pdf.

[12] Department of Work and Pensions (n. 9).

[13] Department for Work and Pensions. (2017). “Automatic Enrolment review 2017: Maintaining the momentum.” https://www.gov.uk/government/publications/automatic-enrolment-review-2017-maintaining-the-momentum.

[14] Pensions Policy Institute. (2020). “The Underpensioned Index.” https://www.pensionspolicyinstitute.org.uk/media/3679/20201208-the-underpensioned-index-report-final.pdf.

[15] Ibid.

[16] The People’s Pension. (2020). “Measuring the Ethnicity Pension Gap.” https://www.abi.org.uk/globalassets/files/publications/public/lts/2022/automatic-enrolment-what-will-the-next-decade-bring/.

[17] Association of British Insurers (n. 1).